Exxon Mobil CEO expects higher oil prices due to I...

2 hours ago

Japanese Prime Minister Sanae Takaichi will make her first official visit to Australia in early May, with Australia’s domestic gas policy likely to be on the agenda. With the Australian government currently designing a new gas reservation scheme, and reportedly having requested Treasury modelling on changes to taxation settings on gas exports, Ms Takaichi is likely to reiterate previous Japanese opposition to changes to our domestic gas policy.

Warnings about Australia’s policy settings are part of a larger lobbying effort. A recent report found that range of Japanese companies and industry bodies have directly lobbied the Australian government to ensure continued supply of liquefied natural gas (LNG).

Less attention has been given to what this lobbying means for Australia’s own gas supply security. The Australian Energy Market Operator (AEMO) forecasts gas shortfalls in eastern and Western Australia this decade, which are more likely to eventuate if Australia maintains or increases exports. The Australian government has already flagged gas market reform, including gas reservation, to address supply concerns.

Lobbying by the Japanese government and companies may reflect energy security concerns, at least in part, but it is also clearly motivated by commercial opportunities. In recent years Japanese companies have invested in LNG import and gas infrastructure across South and South-East Asia as part of government plans to increase LNG demand across the region, with LNG sales by Japanese companies increasing over recent years.

IEEFA’s analysis clearly shows that, while proposed changes to domestic gas policies may pose a threat to Japan’s commercial interests, they will not impact on its energy security.

A recent survey published by the Japanese Organisation for Metals and Energy Security found that Japan’s LNG resales in FY2024 reached record levels of almost 44 million tonnes (Mt), equivalent to about 1.7 times the volumes that Japan imported from Australia. A material portion of this LNG came from Australia.

Japanese companies continue reselling large volumes of Australian LNG

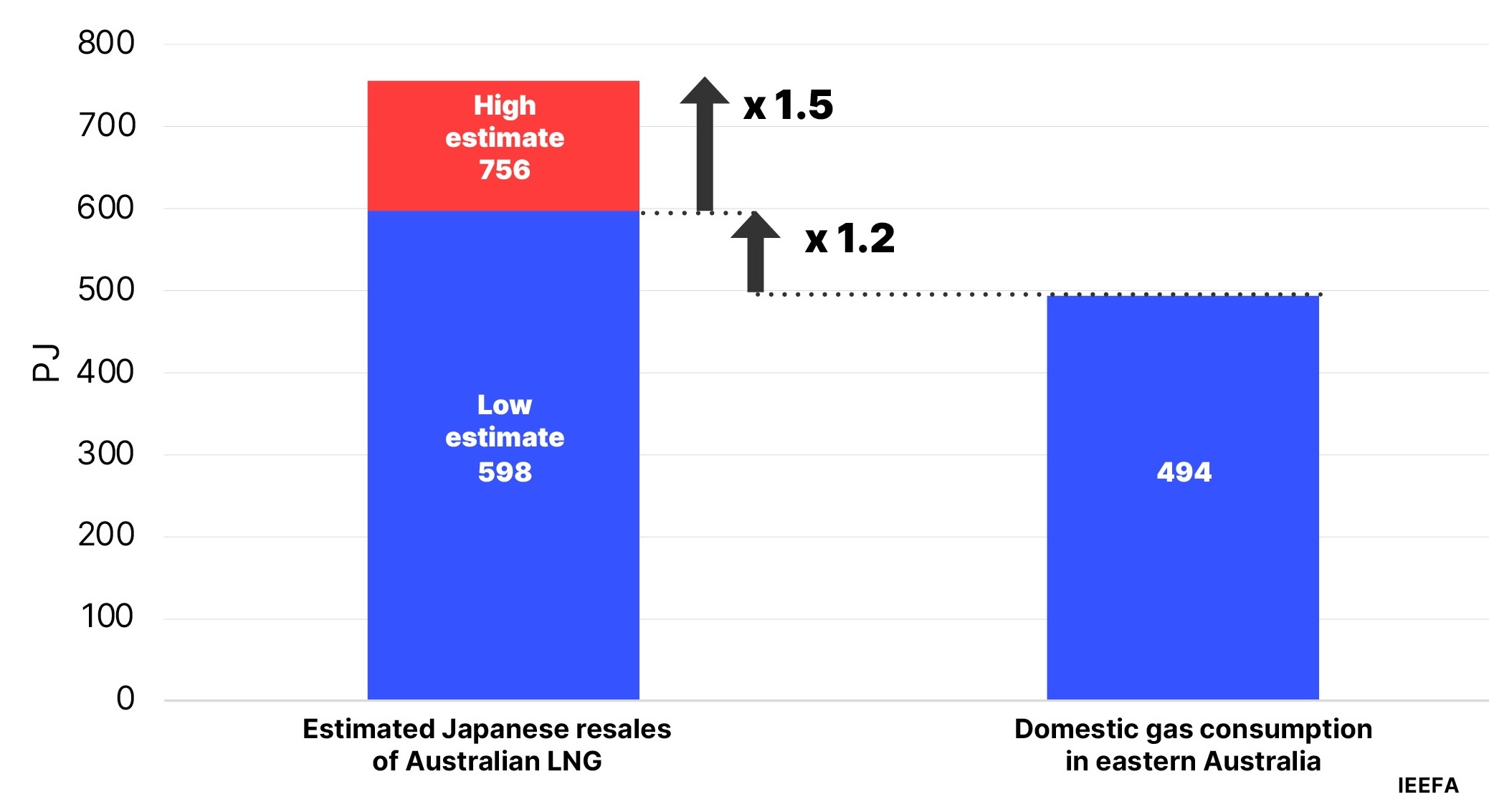

In 2025, Japanese companies sold an estimated 598-756 petajoules (PJ) of Australian LNG into markets outside Japan (Figure 1), down from estimated resales of 627-812PJ in 2024. Resales in 2025 comprised the following (our methodology is set out here):

• 369PJ of Australian LNG transported to third countries on ships chartered by Japanese companies (trackable resales, identified using reliable ship tracking data).

• An estimated 229PJ of contracted LNG transported by the Australian LNG seller to a buyer outside Japan on behalf of a Japanese company (high confidence).

• An estimated 158PJ of spot LNG from Australia sold by Japanese companies but transported by the Australian seller into a third country (low confidence).

Japanese company resales of Australian LNG in 2025 were materially higher than demand in Australia’s eastern states (494PJ) or in Western Australia (381PJ).

Source: IEEFA analysis, Kpler, ICIS, AEMO.

Notably, actual LNG flows from Australia to Japan in 2025 were practically identical to the volume of LNG contracted with Japanese buyers. This suggests Japanese companies also purchased LNG spot cargoes (with the LNG coming from Australia) to replace the volumes of Australian LNG sold into other markets.

IEEFA also estimates that about 26% of the Australian LNG resold into other markets was purchased from Australia on a spot basis, highlighting the discretionary trading role played by Japanese companies.

Australia is the second-largest source of LNG resold by Japanese companies

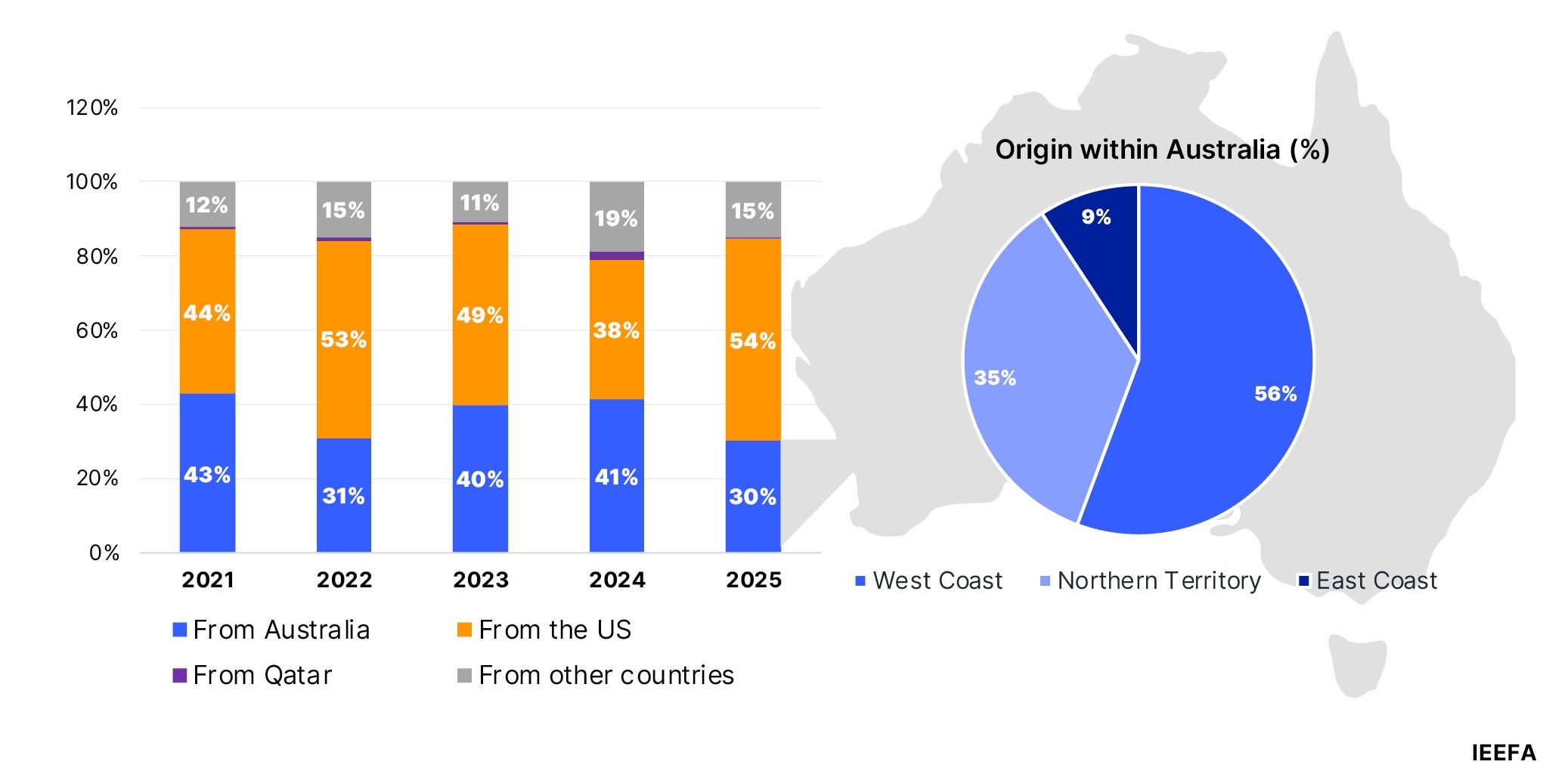

Based on trackable resales, Australia was the second-largest source of LNG resold by Japanese companies in 2025, accounting for 30% of LNG resales. This is a material drop in the share of resales coming from Australia, which represented 41% of resales in 2024. Australia was second only to the US, which is not surprising given the ramp-up in US LNG supply and the inherent flexibility embedded in new US LNG contracts (which allow LNG buyers to sell LNG into any market).

In contrast, resales of LNG from Qatar accounted for only 1% of Japanese company resales, with all other suppliers accounting for 15%.

Source: IEEFA analysis, Kpler.

Within Australia, just over half of LNG resold via ships chartered by Japanese companies was from Western Australia, followed by the Northern Territory, which accounted for about a third. This reflects much higher levels of investment and contracted volumes from those jurisdictions. Queensland, on other hand, accounted for just under 10% of LNG resales transported on ships chartered by Japanese companies.

Japanese companies primarily sell Australian LNG into premium markets

The majority of Japanese resales of Australian LNG were into wealthier markets.

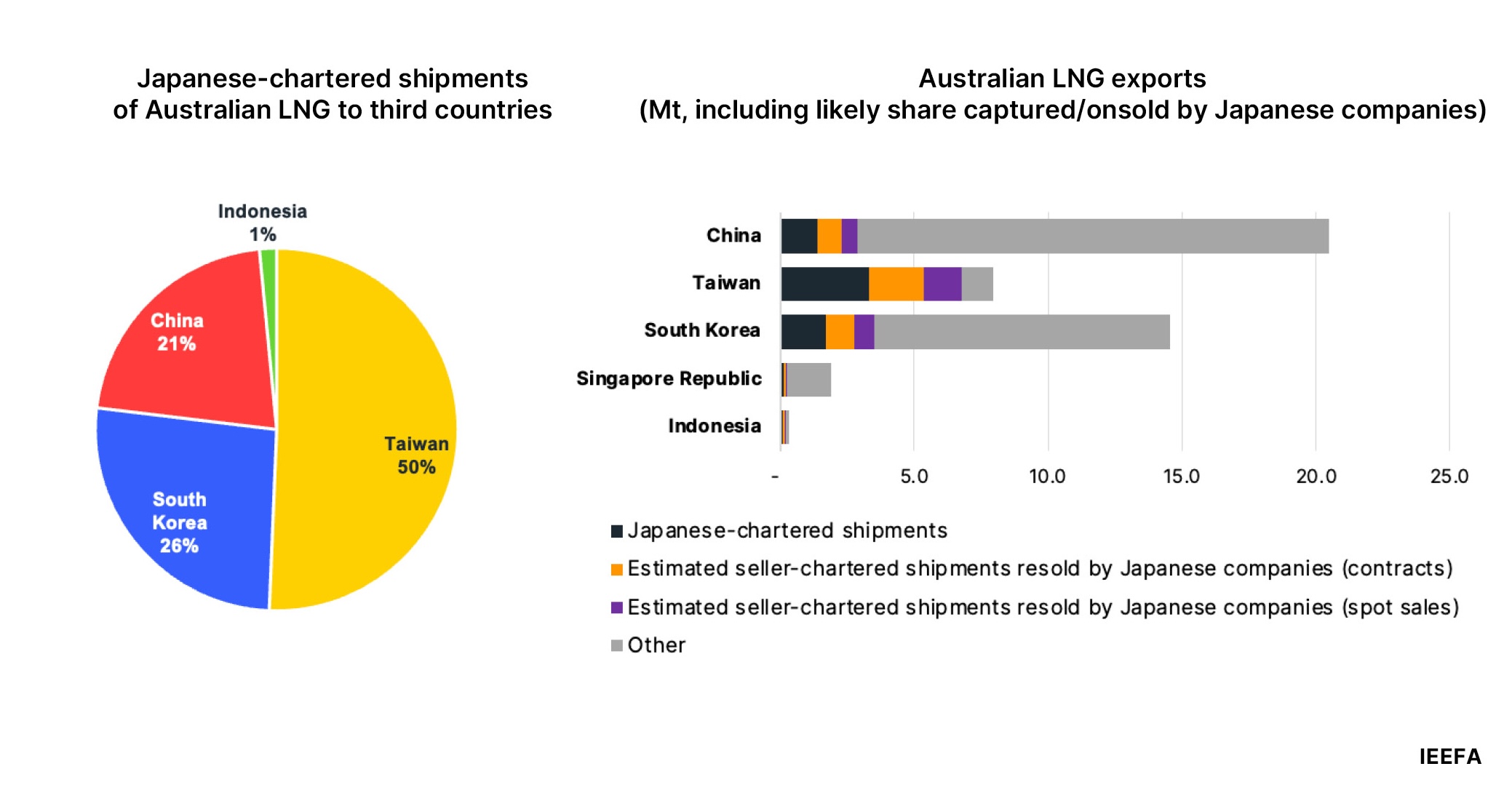

In 2025, about half of Japan’s resales of Australian LNG (where the Japanese company transported the cargo) went to Taiwan (Figure 3), which likely reflects fuel switching due to the closure of Taiwan’s remaining nuclear energy facilities. Japanese LNG resales to Taiwan were so large that they accounted for the vast majority of Australian LNG flowing to Taiwan.

South Korea and China were the next largest destinations, accounting for 49% of trackable resales, followed by Indonesia, which accounted for only 1%.

Source: IEEFA analysis, Kpler, ICIS.

The importance of Australian LNG for Japan’s energy security will almost certainly be raised when the Japanese Prime Minister arrives for her visit. However, amid emerging supply security concerns, it is crucial that Australian policy-makers recognise the commercial motivations underpinning Japan’s lobbying. Australia can implement a domestic gas policy that ensures security of supply at home without impacting on Japan’s energy security.

The only question is whether policy-makers will have the courage to protect domestic gas users.

Source: IEEFA