Borr Drilling’s CEO: Middle East conflict brings u...

7 hours ago

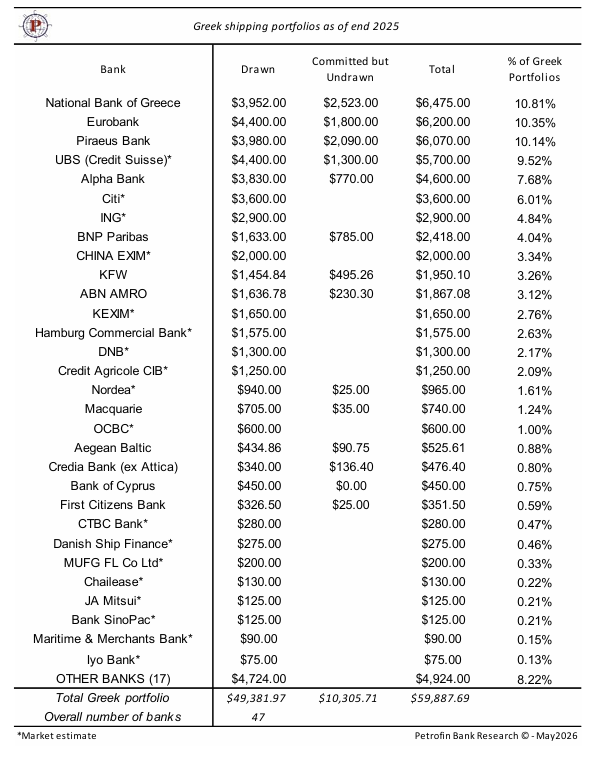

Bank ship finance for Greek shipping recorded a very impressive leap with Greek banks emerging in 2025 as the absolute protagonists of the market.

The latest report of Petrofin Research shows that the bank ship finance for Greek shipping increased from 5% in 2024 to 11.5%, bringing the overall Greek loans (both drawn and committed but undrawn) booked both in Greece and worldwide to a total of $59,687.69m as of end 2025. This was the second consecutive year of growth, from $53,510.88m in 2024, according to Petrofin Research latest report.

According to Petrofin Bank Research, Greek ship finance grew by 11.5% in 2025 from $54.5bn to 59.7bn with the Petrofin Index jumping from 324 in 2024 to 361 as of year-end 2025.

Greek banks were the standout performers, which not only occupied the top 3 places among all lenders to Greek owners, but also recorded a growth from $18.6bn in 2024 to $25bn in 2025 or 34%.

For the first time the National Bank of Greece ended at the very top position of lenders to Greek shipping marking a huge growth of 53%, inclusive of commitments. Eurobank followed in the second place and Piraeus Bank in the third place, while Alpha Bank was in fifth place.

The top 10 Greek ship financing banks stood at $41.91bn compared to $35.98bn in 2024, a significant increase of 16.5%. Their market share shows steady growth reaching 70% for the first time in many years, compared to 67% in 2024.

Petrofin Research attributes the remarkable expansion of Greek banks portfolios to their long-term commitment and sector expertise, earning the trust of owners, especially the medium and smaller operators who value consistent support across market cycles.

Furthermore, the improved credit rating of Greek banks and of Greece itself have enabled Greek banks to offer attractive loan margins and loan fees.

Additionally, Greek banks started to offer large facilities per client for vessels and fleets and especially for newbuildings. As such, Greek owners had an opportunity to borrow not only from the major international banks, but also from Greek banks which invariably provided loans on their own books and not via syndications or joint deals.

Moreover, Greek banks developed numerous ancillary services and further sources of income for their clients involving FX, interest hedging, private banking, investment products, real estate lending, hotel lending, as well as the use of the banks’ retail, deposits and various products.

At the same time, international banks without a Greek presence had a drop of 4.3% reversing the previous year’s growth of 2.5%.

International banks, both with and without Greek presence found it increasingly difficult to compete with Greek banks and their combined drawn portfolios showed a modest overall growth of 3%.

The Petrofin Index for Greek Ship finance, which commenced at 100 in 2001 and peaked at 443 in 2008, increased to 361, from 324 in 2024. It should be noted that the Petrofin Index relates to bank related finance only. Finance via SLBs, leasing and other forms of lending are not included.

It is believed that European banks that remain in Greek ship finance are aiming to expand their portfolios further in this sector. Indeed, of the banks involved in Greek ship finance, the vast majority have higher loan portfolio budgets for 2026 and are only limited from growing by competition from non-bank related finance, as well as prepayments due to the high liquidity of Greek owners and high interest rates.

Furthermore, the newbuilding finance share of the forward commitments has increased from 54.5% in 2024 to 58% by the end of 2025.